Digital payments have quietly become the backbone of modern commerce. Behind every tap, swipe, and checkout button is a layer of infrastructure that most people never see. Adyen is one of the companies that built that infrastructure, and it built it in a way that set it apart from almost everyone else in the industry.

This post breaks down exactly how Adyen works, how it makes money, and why it has become one of the most important payment platforms for enterprise businesses worldwide.

What is Adyen?

Adyen is a global payment technology company that allows businesses to accept payments from customers anywhere in the world, through any channel. That means online, in-store, and on mobile, all processed through a single unified platform.

The company was founded in 2006 in Amsterdam, Netherlands by Pieter van der Does and Arnout Schuijff. The name “Adyen” means “start over again” in Surinamese, which reflects the founding team’s intent to rethink how payment infrastructure should work from the ground up.

Before Adyen existed, large businesses had to stitch together multiple payment processors, gateways, and acquirers to handle transactions across different regions and channels. This created fragmented data, inconsistent customer experiences, and a painful amount of operational overhead. Adyen was built to replace all of that with a single, end-to-end platform.

Key facts at a glance:

- Founded: 2006

- Founders: Pieter van der Does and Arnout Schuijff

- Headquarters: Amsterdam, Netherlands

- Listed on Euronext Amsterdam stock exchange since 2018

- Serves major global brands including Spotify, Uber, Netflix, and eBay

How Adyen Works

To understand Adyen’s business model, you first need to understand what actually happens when someone pays for something.

Here is the payment flow in plain terms:

- A customer initiates a payment, whether that is clicking “buy now” online, tapping a card in-store, or paying through a mobile app.

- The merchant’s system sends the transaction request to Adyen.

- Adyen routes the request through the relevant card network, such as Visa or Mastercard.

- The card network contacts the customer’s bank, which either approves or declines the transaction.

- Adyen communicates the result back to the merchant in real time.

- Funds are settled to the merchant according to Adyen’s settlement schedule.

What makes Adyen different is that it handles every step of this process in-house. Most payment companies rely on third-party processors or acquirers for parts of this chain. Adyen built its own acquiring capabilities, which means it has more control, better data visibility, and fewer intermediaries taking a cut.

This same infrastructure handles online payments, in-store point-of-sale terminals, and mobile payments. A retailer with stores in thirty countries and an eCommerce site can run all of their transaction data through one platform and see everything in one place.

Adyen Business Model Overview

Adyen operates as a Payments-as-a-Service platform. It is not simply a payment gateway or a processor. It is both of those things at once, plus a risk management layer, a data analytics engine, and a global acquiring network.

The platform structure includes:

- Payment gateway: Routes transactions from merchant to bank and back

- Payment processor: Handles the technical communication between all parties

- Acquiring: Adyen holds its own banking licenses and acts as the merchant’s acquirer in many markets

- Risk and fraud management: Real-time tools that screen transactions before they are approved

- Data and analytics: A reporting layer that gives merchants visibility into their transaction data globally

- Unified commerce infrastructure: A single platform connecting online, mobile, and physical sales channels

The core appeal of this model is simplicity for enterprise clients. Instead of managing four or five different vendors for payment processing, gateway services, fraud tools, and reporting, a company like Uber can hand all of that to Adyen and get one integration, one data set, and one bill.

This is a fundamentally different approach from most of the payment industry, which has historically been fragmented and dependent on regional providers.

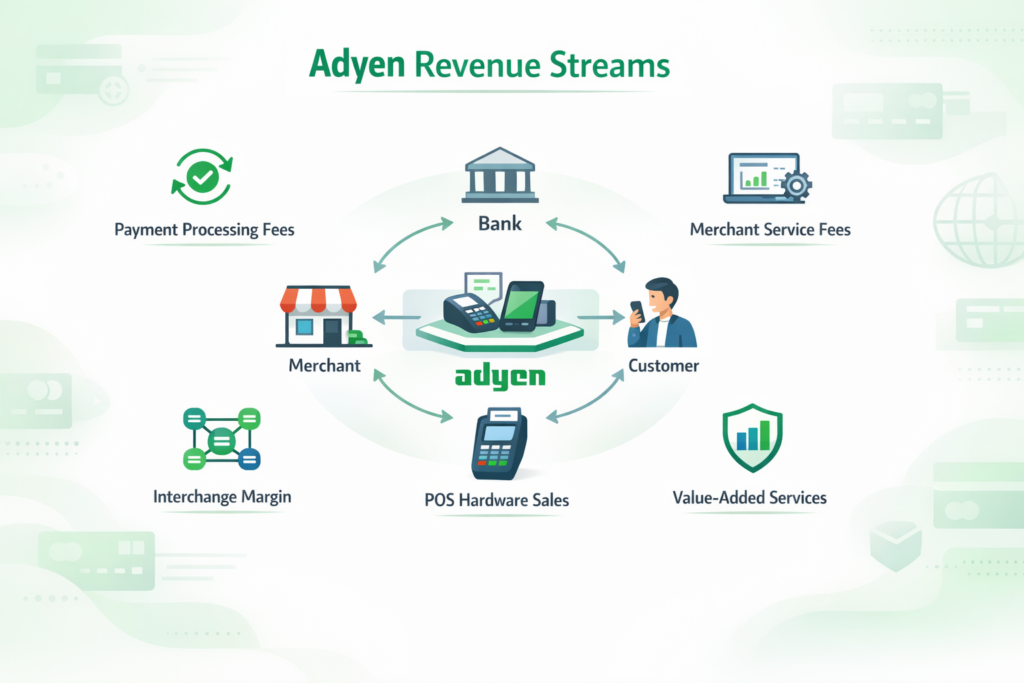

Adyen Revenue Streams

This is the heart of the business model. Adyen generates revenue through several interconnected streams, all flowing from its position as the infrastructure layer in a transaction.

Let’s visualize the flow before breaking each stream down:

Payment Processing Fees

Every transaction that flows through Adyen generates a processing fee. This is the most direct and significant source of revenue.

Adyen charges a flat processing fee per transaction, known as a “processing markup,” plus a small percentage of the transaction value. The exact amount varies by merchant, market, and payment method, but the model is consistent: every time a customer pays through a merchant using Adyen, Adyen earns a fee.

Because Adyen focuses on large enterprise clients with extremely high transaction volumes, even a small per-transaction fee compounds into substantial revenue at scale.

Interchange Plus Network Fees

This is where Adyen’s position as an acquirer becomes particularly valuable. When a card transaction is processed, interchange fees flow from the merchant’s bank through the card network. As an acquirer, Adyen collects these interchange fees and passes the base amount to the card network while keeping a margin on top.

This “interchange plus” model means Adyen earns a spread on every transaction it processes, above and beyond the basic processing fee. The more volume Adyen processes, the more this adds up. It also creates a natural alignment with the card networks, since Adyen’s revenue grows as payment volume grows.

Merchant Service Fees

Businesses that use Adyen also pay fees for accessing the platform itself. This includes:

- Gateway access fees for routing transactions

- Monthly or annual platform usage fees

- Integration and technical support costs

- Fees tied to specific features like tokenization or network tokens

These fees are typically bundled into the overall commercial agreement Adyen negotiates directly with enterprise clients. Because Adyen sells primarily to large businesses rather than small merchants, these agreements tend to be significant in value.

Value-Added Services

Adyen offers a growing set of services that sit on top of the core payment infrastructure:

- Fraud and risk management: Real-time transaction screening powered by machine learning that reduces chargebacks and false declines

- RevenueProtect: Adyen’s proprietary risk engine that uses data across its global merchant base to improve fraud detection

- DataConnect: Analytics tools that let merchants analyze payment performance and customer behavior across markets

- Payment optimization: Adyen’s routing logic dynamically selects the most likely path to authorization for each transaction, which improves approval rates and reduces unnecessary declines

These services generate incremental revenue on top of transaction fees and increase the overall stickiness of the platform. Once a company has integrated fraud tools, analytics, and payment optimization through Adyen, switching to a competitor becomes significantly harder.

POS Hardware and In-Store Payments

Adyen sells and leases point-of-sale terminals for physical retail locations. These terminals are proprietary hardware that connects directly to the Adyen platform, creating the same unified data experience in-store as the company offers online.

Revenue from this stream includes:

- Terminal sales and rentals

- Per-transaction fees on in-store payments

- Subscription fees for terminal management software

For large retailers operating hundreds or thousands of locations, this is a meaningful revenue line for Adyen and a strong lock-in mechanism for the relationship.

Adyen Value Proposition

The reason global companies choose Adyen over competing providers comes down to a few specific advantages that are difficult to replicate:

Global payment support. Adyen supports over 250 payment methods and processes payments in over 150 currencies. For a company like Netflix or Spotify operating in dozens of countries, this eliminates the need to manage regional payment providers in each market.

Unified commerce. Adyen connects online, mobile, and physical payments into a single data stream. A retailer can see the same customer’s purchase history whether they bought online or in a store, using one platform.

Real-time data and reporting. Because Adyen processes the entire transaction chain, it has access to more detailed data than a gateway-only provider would see. This data powers optimization tools, fraud detection, and business intelligence dashboards.

Fraud protection at scale. Adyen’s risk engine improves over time as it processes more transactions. Larger merchants benefit from the aggregated intelligence across the entire platform.

Single integration. A company that integrates Adyen gets global payment coverage, fraud protection, data analytics, and POS capabilities from one codebase and one API.

Major brands that rely on Adyen include Spotify, Uber, Netflix, eBay, Microsoft, McDonald’s, and many others. These are not small businesses that signed up for a self-serve product. They are enterprises that went through a rigorous evaluation process and chose Adyen as a strategic infrastructure partner.

Adyen Customers

Adyen targets three broad customer segments, though it concentrates most of its sales and product development on the first category.

Enterprise businesses are Adyen’s primary market. These are large global companies with complex payment needs across multiple geographies, channels, and currencies. They typically have dedicated integration teams, long contract cycles, and high transaction volumes. Adyen’s sales process is direct and relationship-driven, with dedicated account managers for each major client.

Digital-first companies include apps, platforms, and marketplaces that need a clean, developer-friendly payment integration and global coverage from day one. Businesses in this segment often value Adyen’s API quality and its ability to scale as they grow internationally.

Retail and omnichannel businesses are companies with both physical stores and digital sales channels. They use Adyen specifically because it connects both channels, giving them a single view of customer payment behavior regardless of where the sale happens.

One thing worth noting: Adyen intentionally avoids the small business market. It does not compete directly with Stripe’s self-serve product tier or with Square’s small merchant focus. This keeps its support costs low and its revenue per customer high.

Adyen Competitive Advantage

Several factors make Adyen’s position difficult to displace.

Single platform, built internally. Unlike most payment companies that have grown through acquisitions and stitched together legacy systems, Adyen built its entire technology stack from scratch. This means fewer integration points, fewer failure modes, and faster feature development.

Own the full stack. Adyen holds acquiring licenses in key markets, which means it can process transactions end-to-end without relying on a third-party acquirer. This gives it pricing flexibility, better data, and more control over the authorization flow.

Network effect on fraud data. Every transaction Adyen processes improves its fraud models. A merchant joining the platform benefits from the intelligence gathered across every other merchant, which creates a compounding advantage as volume grows.

Switching costs. Integrating Adyen into a large enterprise payment stack is a significant technical project. Once embedded into core systems, POS hardware, mobile apps, and accounting workflows, replacing it is a major undertaking. This creates natural retention.

Global coverage without a patchwork of partners. Building out payment acceptance in thirty countries typically requires relationships with thirty regional processors. Adyen offers that coverage through one relationship.

Adyen Competitors

Adyen operates in a competitive market, but its focus on enterprise clients means it occupies a somewhat different segment than many of its rivals.

Stripe is probably the most similar company in terms of technology quality and developer experience. Stripe has moved upmarket over time and now competes directly with Adyen for enterprise clients. The two companies are genuine rivals, though Adyen has generally been stronger in omnichannel and POS use cases.

PayPal is a much larger brand in consumer awareness but operates differently as a business. PayPal is primarily a consumer wallet and seller tool, and while it processes enormous volumes, it is not primarily targeting the same large enterprise omnichannel deals as Adyen.

Worldpay is a legacy enterprise processor with global reach and a large existing client base. It competes with Adyen on enterprise deals but is generally seen as a less modern, less unified platform.

Square (now Block) focuses on small to medium businesses and POS solutions. It competes with Adyen on the in-store payments side but does not target the same enterprise market.

Adyen Growth Strategy

Adyen has grown primarily by going deeper with existing customers and adding new large enterprise clients rather than by expanding into lower-margin small business segments.

Enterprise focus. Adyen continues to invest in capabilities that matter to large global businesses: more payment method coverage, better authorization optimization, and richer data tools. The strategy is to become indispensable to the enterprise clients it already has.

Geographic expansion. Adyen is growing its acquiring footprint in markets where it currently relies on third-party acquirers. Adding acquiring licenses in new regions improves margins and gives the platform better data in those markets.

Platform expansion. Adyen has been building out financial services capabilities beyond payments, including embedded banking features for platforms and marketplaces. This opens up new revenue streams and increases how deeply clients rely on Adyen’s infrastructure.

Partnerships. Working with global commerce platforms, enterprise software providers, and system integrators to reach new clients through existing relationships.

Challenges in Adyen’s Business Model

Adyen’s model is strong, but it is not without real risks.

Competition is intensifying. Stripe has explicitly targeted large enterprises, and other players are investing heavily in similar capabilities. The gap between Adyen and well-funded competitors is narrowing.

Regulatory complexity. Payment companies operate under financial regulations in every market they serve. New licensing requirements, data localization rules, and open banking mandates create ongoing compliance costs and can slow expansion into new regions.

Fraud and cybersecurity risks. As a high-value payments target, Adyen faces constant pressure from fraudulent actors. The strength of its risk engine is a competitive advantage, but it also requires continuous investment to stay ahead.

Dependence on global commerce. Adyen’s revenue scales with the volume of commerce flowing through its platform. Economic slowdowns, reduced consumer spending, or disruptions to global trade all directly affect revenue.

Talent and infrastructure investment. Maintaining a proprietary global payments stack requires a large and specialized engineering team. The cost of building and maintaining that infrastructure is a meaningful ongoing expense.

Future of Adyen

Several growth areas look particularly relevant for Adyen’s next phase.

Embedded finance. Adyen’s platform already allows marketplaces and platforms to offer payment services to their users. The next step is enabling those platforms to offer broader financial services, including lending, banking, and insurance products, using Adyen as the underlying infrastructure. This is a significant market opportunity.

Digital wallets and alternative payment methods. Consumer payment preferences are shifting. Adyen is expanding its support for digital wallets, buy now pay later providers, and account-to-account payments. Supporting these methods is critical for maintaining relevance with its merchant base.

Cross-border commerce growth. As more businesses sell internationally, the demand for a single platform that handles multiple currencies, languages, and local payment methods continues to grow. This is Adyen’s home turf.

AI-driven fraud detection and authorization optimization. Adyen is investing in machine learning models that improve authorization rates and reduce fraud in real time. As these models improve, they become a stronger reason for merchants to stay on the platform.

Adyen Business Model Canvas

For a structured view of how the model fits together:

Key partners: Visa, Mastercard, American Express, regional card networks, banking partners in key markets, technology integration partners

Key activities: Transaction processing, acquiring, fraud risk management, platform development, enterprise sales and account management

Value propositions: Single global payment platform, unified online and offline commerce, real-time data and analytics, high authorization rates, enterprise-grade reliability

Revenue streams: Transaction processing fees, interchange margin, platform and gateway fees, value-added services, POS hardware and in-store fees

Customer segments: Global enterprise businesses, digital-first platforms and marketplaces, large omnichannel retailers

Conclusion

Adyen built something that most payment companies have tried and failed to build: a single, unified platform that genuinely works at global enterprise scale across every channel and payment method.

Its business model is straightforward in concept. It sits in the middle of every transaction its clients process, earns a fee on each one, and layers additional revenue on top through services that make merchants more likely to stay and less likely to leave.

What makes the model durable is the combination of high switching costs, a compounding data advantage, and a deliberate focus on the clients with the highest volume and the most complex needs. Adyen does not try to be everything to everyone. It tries to be indispensable to the companies that move the most money.

That focus, combined with the investment in building its own stack from the ground up, is why Adyen has become one of the most important infrastructure companies in global commerce, and why it continues to grow even as competition in the payments industry intensifies.

Discover more from Business Model Hub

Subscribe to get the latest posts sent to your email.