Adobe Inc. makes money primarily through a subscription-based SaaS model, offering creative tools like Photoshop, document solutions like Acrobat, and digital marketing software through monthly and annual plans. It’s one of the cleanest recurring revenue machines in the software industry.

What Adobe Actually Is

Adobe was founded in 1982 and spent its first few decades selling boxed software. Today it’s a cloud-first subscription platform used by over 30 million paying subscribers globally.

Most people know Adobe through its creative tools: Photoshop, Illustrator, Premiere Pro, InDesign, After Effects. But that’s only one-third of the business. Adobe also runs a massive document management platform and an enterprise digital experience division that most consumers never see.

Its users span three broad groups: individual creators and students, small-to-medium businesses, and large enterprises running complex marketing operations. That layered customer base is a big part of why Adobe generates revenue in so many different ways.

Adobe isn’t just a software company anymore. It’s the backbone of the creator economy, the digital document ecosystem, and increasingly, enterprise marketing infrastructure.

The Core Business Model: SaaS Done Right

Adobe’s core model is Software as a Service. Instead of buying a license once, customers pay monthly or annually for continuous access. That means automatic updates, cloud storage, cross-device syncing, and always the latest version of every app.

This shift happened around 2012 and 2013, when Adobe announced Creative Cloud and began migrating its entire product catalog to a subscription model. The transition was painful for a short period but became one of the most successful SaaS pivots in tech history.

What makes Adobe’s SaaS model strong is the combination of recurring revenue, deep product integration, and high switching costs. Customers don’t just pay for one app. They buy into an ecosystem.

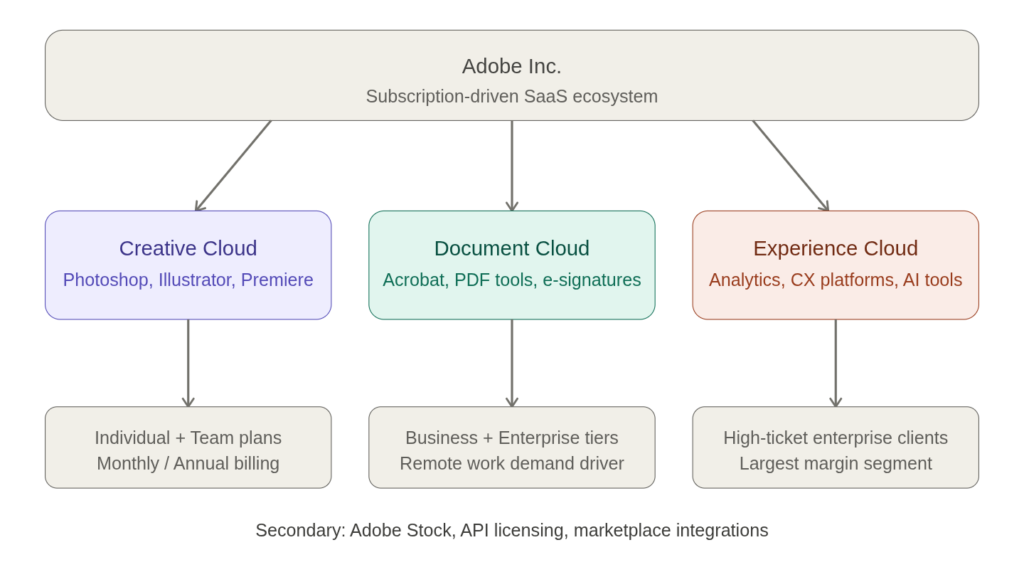

The three main clouds Adobe operates:

Creative Cloud covers all the creative tools. Document Cloud handles PDF and e-signature workflows. Experience Cloud serves enterprise marketing teams with data, analytics, and personalization platforms.

Each cloud has its own pricing structure, its own customer segment, and its own growth trajectory. Together, they make Adobe’s revenue surprisingly diversified for a company most people think of as “the Photoshop company.”

How Adobe Actually Makes Money: Revenue Streams Explained

Creative Cloud: The Main Engine

Creative Cloud is Adobe’s largest and most recognized revenue source. It bundles over 20 apps under one subscription: Photoshop, Illustrator, Premiere Pro, After Effects, InDesign, Lightroom, and more.

Pricing is tiered. Individual users can subscribe to a single app or the full suite. Businesses pay per seat with team-level collaboration features. Enterprise plans get custom pricing, admin controls, and dedicated support.

The key dynamic here is that professionals have no real alternative. Photoshop isn’t just a product. It’s an industry-standard workflow. When hiring managers post “Photoshop experience required,” Adobe wins by default. That brand entrenchment translates directly into pricing power.

Individual all-apps plans run around $54.99/month in the US at standard pricing, though Adobe runs frequent promotions and educational discounts. For a company, that cost per seat across a team adds up fast. Multiply that globally across 30 million subscribers and you get why Creative Cloud alone generates billions per year.

Document Cloud: Quietly Massive

Most people underestimate Document Cloud. Adobe Acrobat has been the global standard for PDF creation, editing, and management for decades, and the shift to remote and hybrid work made that position even stronger.

Beyond PDFs, Document Cloud includes Adobe Sign, which competes directly with DocuSign in the e-signature market. Businesses pay to send, track, and legally sign documents at scale.

The demand driver here is institutional. Law firms, financial institutions, government agencies, HR departments, all of them run on PDF workflows. Moving away from Acrobat isn’t just an inconvenience. It’s a compliance and workflow restructuring project. That stickiness keeps renewal rates high.

Document Cloud is growing steadily, driven by digitization of paperwork in industries that were slow to modernize. It’s not flashy, but it’s predictable and profitable.

Experience Cloud: The Enterprise Juggernaut

Experience Cloud is the part of Adobe most consumers never encounter, but it’s where some of the highest-margin revenue comes from.

This is Adobe’s digital marketing and customer experience platform. It includes tools for analytics (Adobe Analytics), content management (Adobe Experience Manager), marketing automation (Adobe Marketo Engage), customer data platforms, and AI-driven personalization.

The target customer here is large enterprises: retailers, banks, airlines, media companies. These organizations need to manage customer journeys across websites, mobile apps, email, in-store, and more. Adobe Experience Cloud ties that together.

Deals at this level can run into seven figures annually. Enterprise software contracts are sticky by nature. Switching a marketing tech stack after it’s been integrated into a company’s operations is a years-long project with massive costs. That means once Adobe lands an enterprise account, it tends to keep it.

Adobe Stock

Adobe Stock is a marketplace for images, videos, vectors, templates, and 3D assets. Customers can buy individual assets or pay a monthly subscription for a set number of downloads.

What makes this sticky is integration. Stock assets can be licensed and dropped directly into Photoshop, Illustrator, or Premiere Pro without leaving the app. That convenience keeps Creative Cloud users from defaulting to competitors like Shutterstock or Getty.

Adobe also pays contributors, creating a supply-side flywheel. More contributors mean more content, which means more reasons for subscribers to stay within the Adobe ecosystem.

Licensing and API Integrations

Adobe generates additional revenue through enterprise licensing deals and API-based services. This includes access to Adobe’s document generation APIs, PDF services APIs, and embeddable tools that let other businesses build Adobe functionality into their own products.

This is a smaller line item but grows as Adobe’s developer ecosystem expands. It’s also strategically important because it extends Adobe’s reach beyond its own apps into third-party platforms.

Pricing Strategy: Why It Works So Well

Adobe’s pricing is built around three core principles.

First, tiered access. Every product has an individual plan, a business plan, and an enterprise tier. This captures customers at every level of willingness to pay, from a freelance graphic designer to a Fortune 500 marketing department.

Second, bundling. The Creative Cloud all-apps plan is positioned as the obvious choice because the per-app cost is substantially higher. Someone who needs Photoshop and Premiere Pro and Illustrator quickly does the math and opts for the bundle. Adobe wins more revenue per customer, and the customer feels they’re getting value.

Third, monthly affordability. Paying $21.99/month feels very different from paying $600 upfront for a perpetual license. Lower friction at the point of purchase means more conversions, especially among individuals and small businesses. Over three years, the subscription customer pays far more than the one-time buyer ever did.

There’s also localized pricing across markets. Adobe adjusts prices based on purchasing power in different countries, making it accessible in emerging markets while still monetizing at full rates in higher-income countries.

The Subscription Shift: Why This Changed Everything

Before 2013, Adobe sold software the old-fashioned way. Photoshop CS6 cost around $700 for a perpetual license. Upgrades cost extra. Piracy was rampant because the upfront cost was prohibitive.

The move to Creative Cloud subscription changed all of that. Here’s what it actually did for the business:

Piracy dropped significantly. When a monthly subscription costs less than a restaurant dinner, the motivation to pirate disappears for most users. Cloud-based license validation also made unauthorized access harder.

Revenue became predictable. Instead of lumpy sales cycles tied to new product launches, Adobe gained a smooth, forecastable revenue stream. This is enormously valuable for planning, hiring, and R&D investment.

Retention became the new growth lever. In subscription models, keeping a customer is as important as acquiring one. Adobe invested heavily in making its products indispensable, which meant faster feature shipping, better integration across apps, and stronger customer support.

Updates got continuous. Customers on the old model often skipped upgrade cycles. Subscription customers always run the latest version, which means Adobe can deprecate old features, ship new ones, and move the whole user base together.

The transition was initially met with backlash from power users who didn’t want to pay perpetually. But within two years, subscriber numbers climbed dramatically and revenue stabilized at a higher baseline than the old model ever delivered.

Adobe’s Growth Strategy

Ecosystem Lock-In

Adobe’s strategy has always been to build tools that work better together than any alternative can match. Illustrator files open natively in Photoshop. Premiere Pro integrates with After Effects. Acrobat connects to Adobe Sign. That cross-product integration creates a workflow that’s genuinely hard to replicate elsewhere.

Every new user who learns one Adobe tool becomes more likely to pick up another. Every team that standardizes on Creative Cloud for design and Document Cloud for approvals is deeper inside the ecosystem. Switching costs compound over time.

The Creator Economy Play

Adobe has strategically aligned itself with the growth of content creation. YouTubers, podcasters, social media creators, game designers, motion graphics artists. These communities didn’t exist at scale 15 years ago. Now they’re massive, and many of them use Premiere Pro, After Effects, or Audition daily.

By keeping professional-grade tools accessible via monthly subscription, Adobe brought in a generation of creators who might have turned to free alternatives. Now they’re subscribers, and many will stay subscribers for their entire career.

Adobe Firefly and AI Integration

Adobe launched Firefly, its generative AI suite, in 2023 and has been integrating it across Creative Cloud apps. Generative fill in Photoshop, text-to-image in Illustrator, AI audio tools in Premiere.

Crucially, Adobe trained Firefly on licensed content, including Adobe Stock, to avoid the intellectual property issues that plague other AI image generators. That matters for enterprise clients with legal exposure concerns.

AI features are becoming a meaningful selling point, especially at the enterprise level. The more AI capabilities Adobe adds, the harder it becomes for smaller competitors to keep up.

Enterprise Expansion via Experience Cloud

Experience Cloud is growing faster than Creative Cloud in percentage terms because the total addressable market is enormous. Every major company in every industry needs to manage customer data, run personalized marketing, and measure digital performance.

Adobe competes with Salesforce, SAP, and Oracle in this space. Winning enterprise accounts in this segment requires deep sales relationships and long procurement cycles, but once won, these accounts rarely churn.

Competitive Advantages: What Makes Adobe Hard to Displace

Industry-standard status. Photoshop is a verb. When creative professionals describe photo editing generically, they say “photoshopping.” That level of brand integration into professional vocabulary is extraordinarily rare and incredibly durable.

High switching costs. Designers spend years learning Adobe workflows, keyboard shortcuts, panel configurations, and plugin ecosystems. Moving to a different tool means relearning everything, and in a deadline-driven industry, that’s a real cost.

Integrated ecosystem. No single competitor covers creative tools, document management, and enterprise marketing in one platform. Canva handles simple design. Figma handles UI/UX. Neither touches the breadth Adobe covers across all three clouds.

Enterprise relationships. Large organizations that use Experience Cloud often also use Creative Cloud and Document Cloud. Adobe sells across departments, which deepens the relationship and raises switching costs at the organizational level.

Content-safe AI. Firefly’s licensed training data gives Adobe a compliance edge in enterprise AI adoption, where legal teams are increasingly scrutinizing AI-generated content for IP risk.

Who Adobe Competes With

Canva has grown aggressively in the beginner and SMB design market. Its drag-and-drop simplicity and free tier attract users who find Photoshop overwhelming. Canva doesn’t threaten Adobe among professionals, but it does capture users who might otherwise have become entry-level Adobe subscribers.

Figma became the dominant tool for UI/UX design, a space where Adobe’s XD product underperformed. Adobe actually attempted to acquire Figma for $20 billion in 2022, but the deal was blocked by regulators in late 2023. Figma remains Adobe’s most direct competitive threat in the design-for-digital category.

CorelDRAW maintains a presence among vector illustration professionals, particularly in manufacturing and sign-making industries, but has significantly smaller market share than Illustrator.

Affinity products from Serif offer one-time purchase alternatives to Photoshop and Illustrator at much lower price points. They’ve attracted professional users who are philosophically opposed to subscription pricing. Still niche, but growing.

The consistent pattern: competitors capture specific niches, but none of them match Adobe’s breadth or its depth in professional workflows.

Real Challenges Adobe Faces

Pricing friction. A full Creative Cloud all-apps subscription costs over $600/year for individuals. In many markets, that’s a significant barrier. Adobe has responded with student pricing and free trials, but pricing remains a point of contention, especially among users who only need one or two apps.

Competition from free tools. GIMP, Inkscape, DaVinci Resolve, and Canva’s free tier all take potential subscribers out of Adobe’s funnel. For casual users, free tools are often good enough. Adobe’s answer has been to add enough professional-grade features that free alternatives feel inadequate once someone’s skills develop.

Learning curve. Photoshop and Premiere Pro are powerful and complex. That complexity is a selling point for professionals but a barrier for new users. Canva’s explosive growth is partly a response to users who found Adobe too steep to climb. Adobe has tried to address this with simplified modes and tutorials, but the core products are still built for experts.

Regulatory scrutiny. The failed Figma acquisition demonstrated that Adobe’s scale now draws close attention from antitrust regulators. Future acquisitions will face significant hurdles, which limits how Adobe can grow through M&A.

Generative AI competition. Midjourney, Runway, and other AI-native creative tools are competing for creative workflows that once required Adobe products. If AI generation becomes good enough for professional output, it could disrupt some of the creative work that currently requires Creative Cloud.

Key Takeaways for Founders and Builders

Adobe’s business model is one of the clearest playbooks in B2B software. A few things worth internalizing:

Subscription beats perpetual licensing for long-term revenue. Yes, the upfront revenue looks smaller. Yes, some customers push back. But recurring revenue compounds, improves forecasting, and builds a more defensible business over time.

Ecosystem beats individual products. Adobe doesn’t win because Photoshop is unbeatable. It wins because Photoshop plus Illustrator plus Premiere plus Acrobat plus Stock creates a switching cost that no single-product competitor can overcome.

Retention is the metric that matters. Customer acquisition gets all the attention in startup culture. Adobe’s real edge is that its customers stay. Net revenue retention above 100% (customers spending more over time) is the goal every SaaS business should be optimizing toward.

High switching costs are a legitimate moat. Some founders treat switching costs as anti-customer. Adobe shows that when switching costs exist because the product is genuinely integrated into someone’s workflow, it’s a competitive advantage that compounds year over year.

Pricing power comes from indispensability. Adobe has raised prices multiple times on Creative Cloud subscriptions. Subscribers grumble, and most of them stay. That’s what pricing power looks like in practice.

Conclusion

Adobe is not a design company. It’s a recurring revenue ecosystem that happens to make design tools. Its real business is building software so deeply embedded in professional workflows that leaving feels more expensive than staying.

The Creative Cloud subscription model generates predictable billions annually. Document Cloud sits at the center of how the world manages paperwork. Experience Cloud serves the enterprises that need to understand and engage their customers at scale.

Adobe’s shift from one-time sales to subscriptions didn’t just change its revenue model. It changed how it thought about every part of its business, from product development to customer success to pricing. The result is one of the most financially resilient software companies ever built.

For anyone studying how to build a business that lasts, Adobe’s model is worth spending serious time on. Subscription infrastructure, ecosystem lock-in, and relentless focus on professional-grade tools. That combination is harder to build than it looks, and harder to compete with once it’s established.

FAQs

Adobe makes money through subscription plans for its three cloud platforms: Creative Cloud for design and video tools, Document Cloud for PDF and e-signature services, and Experience Cloud for enterprise marketing software. Subscriptions account for the vast majority of revenue.

Creative Cloud is Adobe’s largest revenue driver. It bundles over 20 professional apps including Photoshop, Illustrator, and Premiere Pro into monthly and annual subscription plans for individuals, teams, and enterprises.

Adobe announced Creative Cloud in 2011 and began transitioning from perpetual software licenses to subscriptions in 2012 and 2013. By 2015, the subscription model was the primary business.

Yes. Adobe Stock generates revenue through pay-per-download and subscription access to photos, videos, and creative assets. Adobe also earns from enterprise licensing deals and API-based developer services, though these are smaller portions of total revenue compared to cloud subscriptions.

In creative tools, Canva (simple design), Figma (UI/UX), and Affinity products are the main alternatives. In enterprise marketing, Adobe competes with Salesforce, SAP, and Oracle. In document management, DocuSign competes in the e-signature segment.

Very much so. Adobe’s operating margins consistently run in the mid-30% range, which is strong for a company of its scale. The subscription model generates high-margin recurring revenue with predictable churn rates, making it one of the more financially efficient businesses in enterprise software.

Discover more from Business Model Hub

Subscribe to get the latest posts sent to your email.