There is a quiet giant sitting inside your banking app. You probably use it without thinking much about it. No fees, no wallet to top up, no app to download separately. Just open your bank, tap a few buttons, and money moves instantly. That giant is Zelle, and the story of how it got there is one of the most interesting strategic plays in modern fintech.

Zelle does not try to make money directly from you. And that is exactly why it wins.

What Is Zelle?

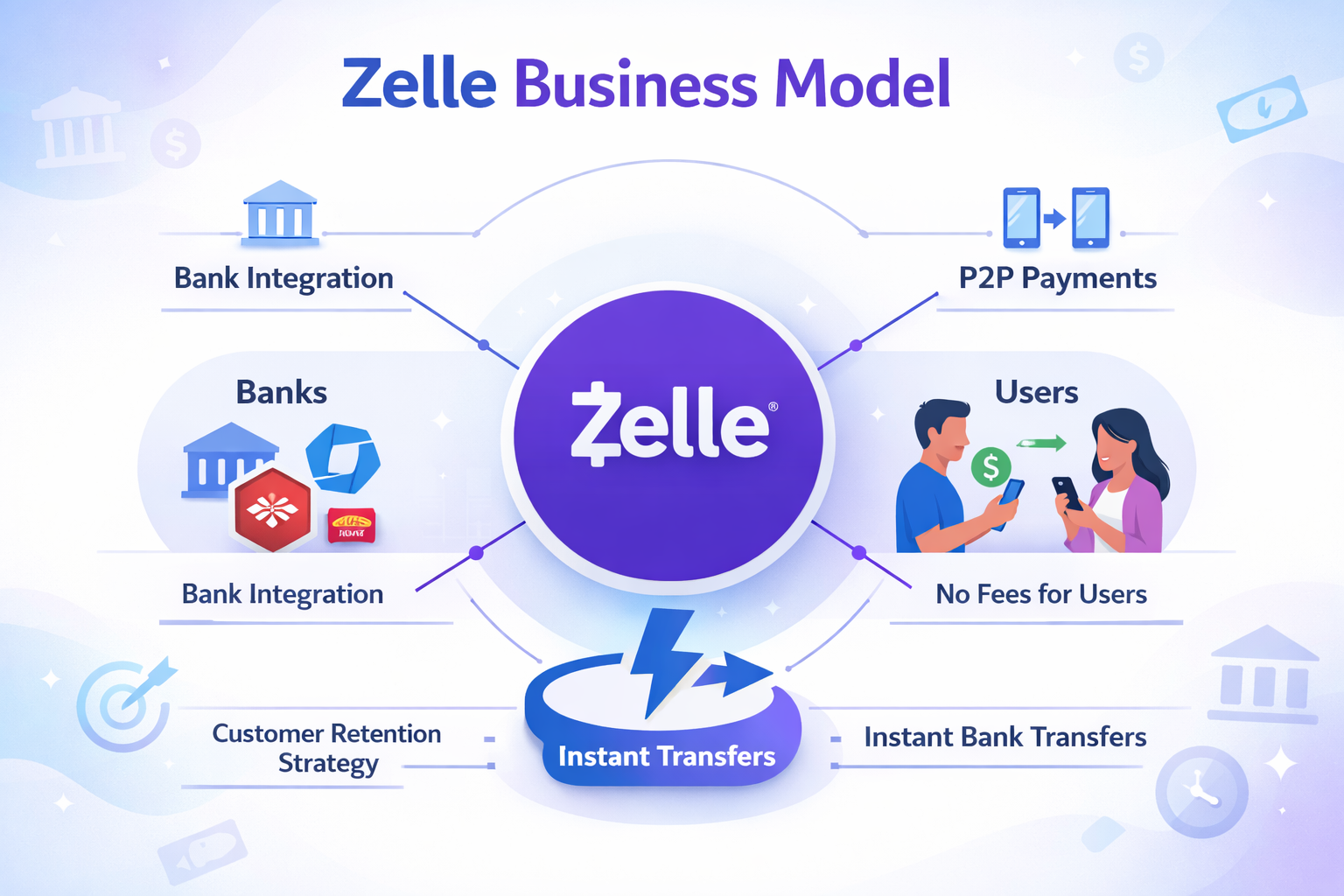

Zelle is a peer-to-peer payment platform that lets users send money directly from one bank account to another in real time. Unlike Venmo or Cash App, Zelle does not hold your money in a digital wallet. There is no balance to manage, no card to reload. Money moves bank-to-bank, instantly.

What makes Zelle structurally different from every other payment app is who built it. Zelle is owned and operated by Early Warning Services (EWS), a company backed by seven of the largest banks in the United States:

- Bank of America

- JPMorgan Chase

- Wells Fargo

- U.S. Bank

- Truist

- PNC Bank

- Capital One

This is not a startup that raised venture capital and built a product hoping banks would one day partner with it. Zelle was created by the banks themselves, for the banks. That distinction shapes everything about how it operates and how it makes money.

The Problem Banks Were Trying to Solve

To understand Zelle’s business model, you have to understand the moment it was born into.

By the mid-2010s, Venmo had become a cultural phenomenon. Millennials were splitting dinner bills, paying rent, and sending birthday money through an app that had nothing to do with their bank. Cash App was rising. PayPal was dominant. Google Wallet was experimenting. Apple Pay was launching.

Banks were watching users do all of their everyday financial activity inside someone else’s app. That is a serious problem, not just because of the revenue those third-party apps were generating, but because of something far more strategic: engagement. Every time a user opens Venmo instead of their bank app, the bank loses a touchpoint. They lose visibility. They lose the chance to cross-sell a loan, a credit card, a savings account.

The banks were not losing money on peer-to-peer transfers. They were losing relevance.

Zelle was their answer.

The Core Idea: Retention Over Revenue

Zelle’s business model is built on a principle that sounds almost paradoxical for a financial product: do not charge users anything, and do not try to monetize the transaction directly. Instead, keep users inside the banking ecosystem where the bank can serve them in ways that actually generate revenue.

This is called a retention strategy. Rather than building a revenue-generating product, the banks built an infrastructure product designed to make their own apps stickier and more competitive.

The logic is straightforward:

- If you can send money instantly from your bank app for free, why would you use Venmo?

- If Venmo is not in your life, your bank app becomes your go-to financial interface.

- If your bank app is your go-to interface, you see mortgage offers, credit card promotions, and savings account nudges far more often.

- That is where the real money is.

Zelle is not a product competing for transaction fees. It is a defensive wall keeping users from walking out the door.

How Zelle Actually Works

The mechanics are elegantly simple, which is part of why adoption spread so quickly.

A user opens their banking app, navigates to the Zelle section (which is built directly into the app), enters the recipient’s phone number or email address, types an amount, and hits send. The money arrives in the recipient’s account within minutes, sometimes seconds.

Behind the scenes:

- There is no intermediary wallet. Money does not sit in a holding account.

- Transfers settle directly between bank accounts using the participating banks’ existing infrastructure.

- Zelle acts as the rail connecting banks, not as a bank itself.

- Fraud detection, verification, and settlement all run through Early Warning Services’ shared network.

Because there is no wallet layer, Zelle cannot offer some of the features fintech apps do, like instant merchant payments or crypto purchases. But it also means there is zero friction for the user. The money they send comes directly from their checking account, and the money they receive lands directly in theirs.

How Zelle Makes Money

This is where most people get confused. If Zelle charges users nothing, where does the revenue come from?

The answer lies in understanding who Zelle’s actual customers are. Zelle’s customers are not the people using the app. Zelle’s customers are the banks.

Bank membership and participation fees. Financial institutions pay to join the Zelle network. When a bank integrates Zelle into its app, it is licensing access to Early Warning Services’ infrastructure. Smaller community banks and credit unions that want to offer Zelle to their customers pay fees to participate. This is the most direct revenue line for EWS.

Transaction cost savings passed back to member banks. For the founding banks, Zelle represents a dramatic reduction in the cost of processing everyday payments. Wire transfers cost banks meaningful sums to process. ACH transfers, while cheap, are not instant and often take one to two business days. Zelle gives banks an instant transfer option built on shared infrastructure at a fraction of the cost. Those savings accumulate at enormous scale across millions of daily transactions.

Customer retention value. This one does not show up as a line item on a revenue statement, but it is perhaps the most financially significant benefit. When a bank retains a customer who would otherwise have shifted their financial activity to a fintech app, it keeps that customer available for higher-margin products. A checking account customer who stays engaged with the bank app is significantly more likely to take a mortgage, open a credit card, or purchase an investment product from that same institution.

Cross-selling through increased engagement. Every time a user opens their banking app to send money via Zelle, they are exposed to the bank’s other products. Banks spend enormous amounts of money on digital advertising and in-app promotions. Zelle effectively increases the number of times a user opens the bank app, multiplying the organic exposure to these offers without the bank spending a cent more on marketing.

Data and behavioral insights. Transaction behavior is valuable. Banks can observe how often customers use Zelle, what amounts they typically send, and how their payment behavior changes over time. This does not mean selling user data, but it does mean the bank has richer behavioral signals to use when building personalized offers and improving risk models.

Why Zelle Does Not Charge Users

The decision to offer Zelle for free was not accidental or charitable. It was a calculated competitive move.

Venmo, Cash App, and PayPal had built strong network effects over years of being free consumer products. The only way to displace them was to offer something equally free but better integrated into daily banking life. Charging even a small fee would have undermined the entire value proposition before it had a chance to take root.

There is also a trust dimension. Zelle carries the implicit backing of the user’s own bank. If Bank of America is offering it, users assume it is safe, regulated, and reliable in ways that a standalone startup app might not be. That credibility would have been damaged if the bank-backed option cost money while the startup option was free.

The zero-fee model also allowed Zelle to scale incredibly fast. Because banks promoted it within their existing apps to their existing customers, there was no customer acquisition cost. The distribution network was already in place. Banks did the marketing. Zelle just had to work.

Zelle vs. Competitors: A Strategic Comparison

Zelle vs. Venmo

Venmo is social by design. It has a public feed, emoji reactions on payments, and a stored wallet. It is an app people enjoy using. Zelle is purely functional. No social layer, no wallet, no frills.

Where Venmo wins is in features and cultural cachet, especially among younger users. Where Zelle wins is in reach and immediacy. Because Zelle is embedded in banking apps, it does not require a separate download or account setup. If you bank at a participating institution, you already have it.

Venmo also charges fees for instant transfers to a bank account. Zelle does not. That difference matters in everyday use.

Zelle vs. Cash App

Cash App has evolved far beyond peer-to-peer payments. It offers a debit card, stock trading, Bitcoin purchases, and a tax filing feature. It is a financial super-app in the making, generating revenue through a range of services.

Zelle has none of that. It does one thing: move money between bank accounts quickly and for free. That simplicity is a weakness in terms of feature breadth, but it is also a strength. There is nothing to learn, nothing to set up, nothing to go wrong.

Zelle is not trying to replace a bank. It is trying to make your bank better.

Key Takeaway

Zelle is an infrastructure play. Its competitors are building ecosystems. Zelle is quietly making sure that the infrastructure your bank runs on is good enough that you never need those ecosystems in the first place.

How Zelle Grew Without a Marketing Budget

Zelle’s growth strategy is a masterclass in distribution-led expansion.

Most consumer products have to spend heavily to acquire users. They run ads, offer referral bonuses, and invest in brand awareness. Zelle did almost none of that, at least not directly. Instead, it leveraged something most startups cannot buy: an existing installed base of tens of millions of banking customers.

When Bank of America or JPMorgan Chase sent their users a push notification saying “send money with Zelle,” they were not promoting a third-party app. They were promoting a feature of their own product. The trust, the relationship, and the communication channel already existed. Zelle simply plugged into it.

The network effects accelerated from there. The more banks joined, the more users had access. The more users had access, the more useful Zelle became for everyone. By the time smaller banks and credit unions joined, they did so because their customers were asking for it, not because Zelle had convinced them.

Strengths of the Zelle Model

- No customer acquisition cost. Users already exist inside partner banks.

- Instant transfer functionality that genuinely solves a real user need.

- Trust from bank backing that consumer fintech apps have to earn from scratch.

- No transaction fees means rapid, frictionless adoption.

- Deep integration means higher daily app engagement for banks.

- Shared infrastructure across member banks reduces individual costs dramatically.

Weaknesses and Risks

No business model is without its vulnerabilities, and Zelle has notable ones.

Fraud is a serious and growing problem. Because Zelle transfers are instant and irreversible, scammers have found it to be a particularly effective tool. Once money is sent, it is nearly impossible to recover. The Consumer Financial Protection Bureau has pressured banks to take more responsibility for fraud that occurs on the platform, and several large banks have faced scrutiny over their handling of scam-related disputes.

Limited feature set. Compared to Cash App or even Venmo, Zelle feels bare. There is no merchant payment option for small businesses in the way competitors offer, no investing feature, and no card product. Users looking for a financial tool that does more than move money will find it limited.

Geographic constraints. Zelle is effectively a U.S.-only product. International payments are not supported. As the world becomes more financially connected, this is a meaningful gap.

Dependence on bank participation. Zelle’s utility is entirely dependent on both the sender and the recipient banking at participating institutions. If your friend uses a credit union that has not integrated Zelle, the transfer fails. That limits reach in ways Venmo and Cash App, which are standalone apps, do not face.

Key Lessons for Founders and Strategists

Zelle’s story is full of lessons that apply far beyond banking.

You do not always need to monetize the product directly. Zelle generates enormous value for its member banks without charging end users anything. If your product makes adjacent revenue streams significantly more valuable, the product itself does not need a price tag.

Distribution beats product in many markets. Zelle is not the most feature-rich payment app. It is not the most beloved. But it had unparalleled distribution from day one because it launched inside apps that hundreds of millions of people already used. A good product in the right channel beats a great product looking for a channel.

Incumbent advantages are real. The narrative in tech often celebrates startups disrupting legacy industries. Zelle is a story of incumbents fighting back, and winning. When large institutions move with real coordination and genuine commitment to solving a user problem, they can compete effectively with even fast-moving startups.

Infrastructure businesses compound quietly. Zelle does not generate headlines the way flashy fintech apps do. But it processes hundreds of billions of dollars annually and has become the default way Americans move money between bank accounts. Boring infrastructure with massive scale is one of the most durable business models that exists.

The Future of Zelle

Zelle has room to grow in several directions, and Early Warning Services has shown an appetite for expanding the product’s role.

Small business payments are an area of active development. Zelle has historically been limited in how effectively it serves business-to-business or consumer-to-business payments, but there are signals that this is changing. If Zelle can become a reliable small business payment tool, it opens an entirely new use case within the existing banking infrastructure.

Regulatory scrutiny will likely intensify. As fraud losses mount and legislators pay more attention to instant payment systems, Zelle and its member banks will face more pressure to improve consumer protections. How they navigate that will shape both user trust and competitive positioning.

Real-time payment infrastructure is also expanding globally, and the U.S. Federal Reserve’s FedNow system represents a new rail that Zelle will need to coexist and compete with. The relationship between Zelle and FedNow will be one of the defining dynamics in U.S. payments over the next several years.

Feature upgrades to close the gap with fintech competitors remain a possibility, though Zelle has historically resisted feature bloat in favor of simplicity. That may continue to be the right call, or it may become a liability as user expectations rise.

Conclusion

Zelle’s real innovation is not technical. The technology behind instant bank transfers existed before Zelle launched. What was new was the strategy: convincing competing banks to set aside their rivalries, contribute to a shared network, and offer something genuinely useful to their customers for free.

Zelle shows that incumbents do not have to cede ground to fintech disruptors. They can cooperate, build together, and defend their ecosystem with products that are simple, trusted, and genuinely better for users on the dimensions that matter most.

It is tempting to think of Zelle as a payment app. But that misses what it actually is.

Zelle is not a payment app. It is a defensive strategy turned into a product, executed at a scale that no startup could have matched from scratch. And that is a far more interesting story.

Discover more from Business Model Hub

Subscribe to get the latest posts sent to your email.