Alibaba is one of the most misunderstood companies in the world. Most people assume it is just a Chinese version of Amazon. But that comparison misses the point entirely. Alibaba does not sell products. It does not own inventory. It does not pack and ship boxes from a warehouse.

What Alibaba built is something far more powerful: an ecosystem. A self-sustaining, multi-sided platform that connects buyers, sellers, brands, and enterprises, and then monetizes the activity that flows between them.

Understanding how Alibaba makes money is not just an exercise in business analysis. It is a masterclass in platform economics, network effects, and scalable monetization. Whether you are a founder, investor, or strategist, the Alibaba model has lessons worth studying carefully.

What Is Alibaba?

Jack Ma founded Alibaba in 1999 from a small apartment in Hangzhou, China. His original vision was straightforward: help Chinese manufacturers connect with international buyers through the internet.

That original vision has since grown into something far larger. Today, Alibaba Group is a sprawling platform ecosystem that spans:

- Consumer eCommerce (Taobao, Tmall)

- B2B trade (Alibaba.com)

- Cloud computing (Alibaba Cloud)

- Digital payments (Alipay, via Ant Group)

- Logistics (Cainiao)

- Entertainment and media

The key distinction is this: Alibaba is a platform business, not a retailer. It does not compete with the sellers on its platform. It empowers them, and then charges for that empowerment.

This is the foundation of everything.

How Alibaba’s Business Model Evolved Over Time

Alibaba did not arrive at its current model overnight. It evolved in deliberate layers, each one building on the last.

The B2B origins

It started with Alibaba.com, a marketplace connecting Chinese manufacturers with global buyers. Small and medium-sized businesses could list their products, and international buyers could find them. This solved a real problem at scale.

The C2C expansion with Taobao

In 2003, Alibaba launched Taobao, a consumer-to-consumer marketplace similar to eBay. Listings were free. The goal was not immediate revenue but scale. Alibaba wanted to flood the platform with products and attract millions of buyers before monetizing.

This was a deliberate choice that paid off. By making listings free, Alibaba out-competed eBay in China and built an enormous seller base.

The B2C premium layer with Tmall

Once Taobao had scale, Alibaba launched Tmall in 2008. Tmall was designed for established brands and larger merchants who wanted a more premium, trusted shopping environment. Unlike Taobao, Tmall charged commissions and fees. This is where a significant portion of Alibaba’s revenue comes from today.

Cloud and logistics as infrastructure

Alibaba Cloud launched in 2009. Cainiao, the logistics network, came later. These were not separate businesses. They were infrastructure plays designed to strengthen the core platform and open new revenue streams.

The insight that explains everything

Alibaba scaled by layering services, not replacing them. Each new platform or service complemented the existing ones. Taobao fed Tmall. Tmall needed Cainiao. All of it ran on Alibaba Cloud. The ecosystem became self-reinforcing.

The Core Platforms Explained

To understand how Alibaba makes money, you first need to understand what each platform does and who it serves.

Taobao

Taobao is China’s largest consumer marketplace, operating on a C2C model. Individual sellers and small businesses list products for free. There are hundreds of millions of listings across every imaginable category.

Taobao does not charge for listings. Instead, it monetizes through advertising. Sellers compete for visibility, and that competition generates revenue.

Tmall

Tmall is the premium B2C counterpart to Taobao. It hosts established brands, both domestic and international. Think Nike, Apple, L’Oreal, and thousands of others selling directly to Chinese consumers.

Tmall charges annual fees, deposits, and commissions on transactions. It is a more structured and monetized environment than Taobao.

Alibaba.com

This is the original platform, focused on B2B wholesale trade. Manufacturers and suppliers list products in bulk. International buyers, distributors, and retailers source from here.

Alibaba.com operates on a subscription model, where suppliers pay for premium memberships to access verified buyer leads and enhanced visibility.

Alibaba Cloud

Alibaba Cloud (also known as Aliyun) is the cloud computing arm of the group. It offers infrastructure, data storage, AI services, and enterprise software solutions.

It is the fastest-growing segment and competes directly with AWS, Microsoft Azure, and Google Cloud, particularly across Asia.

Cainiao

Cainiao is Alibaba’s logistics network. It does not own fleets or warehouses outright. Instead, it acts as a coordination layer, connecting third-party logistics providers, warehouses, and delivery services into one integrated network.

Cainiao charges for fulfillment, warehousing, and delivery services.

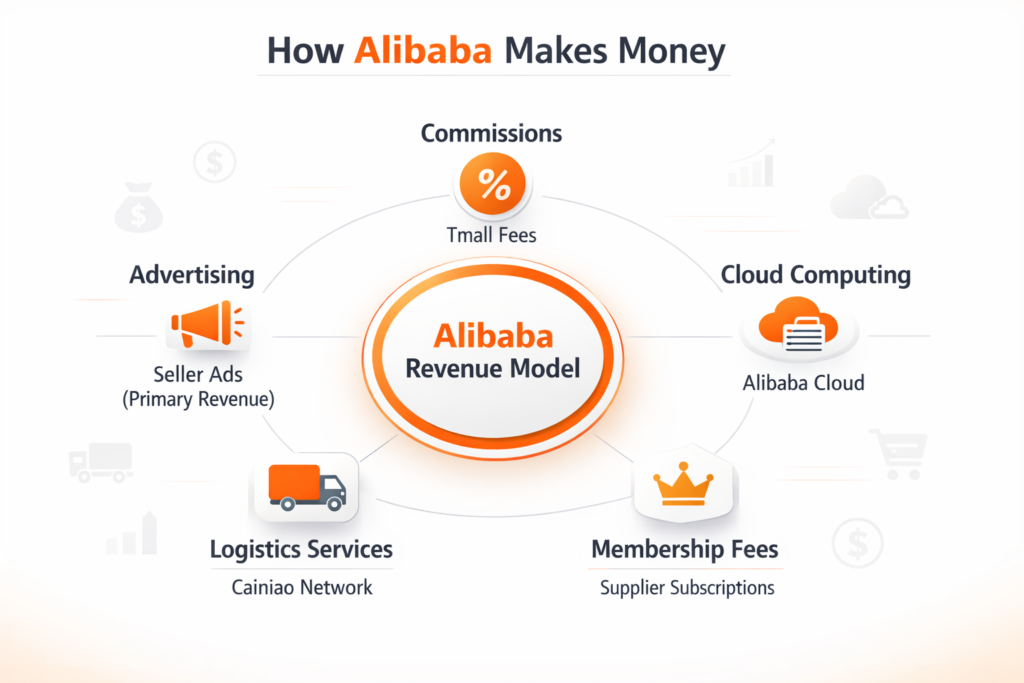

How Alibaba Actually Makes Money

This is the core of everything. Alibaba has five primary revenue streams, each tied to a specific part of its ecosystem.

Advertising: The Primary Revenue Engine

Advertising is Alibaba’s biggest money-maker, and the mechanics are elegant.

Because listings on Taobao are free, millions of sellers compete for the same buyers. The only way to rise above the noise is to pay for visibility. Sellers bid on keywords, pay for promoted placements, and buy banner ads across the platform.

This is essentially a Google-style auction model built into a shopping marketplace. The more sellers on the platform, the more competition. The more competition, the more ad spend. The more ad spend, the more revenue for Alibaba.

Key advertising products include:

- P4P (Pay for Performance): Keyword-based bidding for search visibility

- Display advertising: Banner and visual placements across the platform

- Brand campaigns: Premium promotional packages for Tmall merchants

The genius of this model is that Alibaba does not need to sell anything. It just needs sellers to keep competing, and they will pay for the privilege.

Commissions and Transaction Fees

Tmall charges a commission on every completed transaction. The commission rate varies by category, typically ranging from a fraction of a percent to several percent of the sale price.

Tmall merchants also pay:

- An annual technology service fee (essentially a platform access fee)

- A refundable security deposit

- Category-specific commission rates per transaction

This creates a reliable, recurring revenue stream tied directly to GMV (Gross Merchandise Value). The more sales happen on Tmall, the more Alibaba earns.

Cloud Computing Revenue

Alibaba Cloud generates revenue through subscriptions and usage-based pricing. Enterprises and developers pay for:

- Compute and storage infrastructure

- Database and networking services

- AI and machine learning tools

- Security and compliance products

Cloud revenue is significant not just for its size but for its margin profile and growth trajectory. As enterprises across Asia and globally digitize their operations, demand for cloud infrastructure grows alongside it.

Alibaba Cloud is now the third-largest cloud provider in the world by revenue, behind only AWS and Azure.

Membership and Subscription Fees

Several of Alibaba’s platforms charge for premium access.

On Alibaba.com, suppliers pay for Gold Supplier memberships. These give them verified status, better search rankings, and access to international buyer inquiries. Annual fees vary by market and tier.

On the consumer side, Alibaba has 88VIP, a premium membership program similar to Amazon Prime. Members get benefits across Taobao, Tmall, and other services for an annual fee.

Subscriptions provide predictable, recurring revenue with strong retention characteristics.

Logistics and Fulfillment via Cainiao

Cainiao charges merchants and consumers for logistics services including:

- Last-mile delivery coordination

- Warehousing and inventory storage

- Cross-border shipping management

- Returns processing

As Alibaba pushes into international markets, Cainiao’s cross-border logistics capability becomes increasingly important. It is also a competitive moat, because a merchant deeply integrated into Cainiao’s fulfillment network has significant switching costs.

The Business Model Canvas

Breaking Alibaba down through the Business Model Canvas framework reveals how tightly integrated every element is.

Customer Segments

Alibaba serves multiple distinct groups simultaneously:

- Small sellers and individual vendors on Taobao

- Large brands and retailers on Tmall

- Manufacturers and wholesalers on Alibaba.com

- Enterprises and developers on Alibaba Cloud

- Consumers across all shopping platforms

Value Proposition

Each segment receives a distinct value proposition:

- Sellers get access to hundreds of millions of buyers, advertising tools, and data-driven insights

- Buyers get unmatched product variety, competitive pricing, and a trusted transaction environment

- Enterprises get scalable, cost-effective cloud infrastructure with deep regional expertise

Revenue Streams

- Advertising (P4P, display, brand campaigns)

- Commissions (Tmall transaction fees)

- Cloud subscriptions and usage fees

- Membership fees (Gold Supplier, 88VIP)

- Logistics services (Cainiao)

Key Resources

- Platform technology and algorithms

- Data from billions of transactions

- The seller and buyer base itself

- Cloud infrastructure

Cost Structure

- Technology infrastructure and R&D

- Cloud data center operations

- Marketing and user acquisition

- Logistics coordination

- Regulatory and compliance costs

The Alibaba Flywheel: Why the Model Scales Automatically

The most powerful element of Alibaba’s business model is not any single revenue stream. It is the flywheel, the self-reinforcing growth loop that makes every part of the ecosystem stronger over time.

Here is how it works:

- More sellers join the platform, increasing product variety

- More variety attracts more buyers

- More buyers increase demand and sales for sellers

- Higher seller competition drives more advertising spend

- More ad revenue funds platform improvements

- Better platform attracts more sellers

And the loop repeats, accelerating with each cycle.

This flywheel is why Alibaba does not need to spend heavily on acquiring either sellers or buyers at scale. The ecosystem recruits them. Once the flywheel is spinning, growth becomes largely organic.

The implication for founders is significant. Alibaba’s model does not just generate revenue. It generates momentum. And momentum compounds.

Unit Economics: Why Alibaba Is So Profitable

Alibaba’s profitability is a function of its cost structure, which is fundamentally different from a traditional retailer.

No inventory costs. Alibaba never buys or holds products. There is no cost of goods sold in the traditional sense. Sellers carry their own inventory.

No warehousing at scale. While Cainiao manages logistics, Alibaba itself does not own a sprawling warehouse network the way Amazon does. This dramatically reduces capital expenditure.

High-margin advertising revenue. Ads are essentially pure margin. Once the platform and ad tech are built, each additional dollar of ad revenue has very low incremental cost.

Seller-funded competition. Sellers pay to compete against each other. Alibaba earns from this competition without taking sides or bearing any commercial risk.

The key insight is this: Alibaba does not monetize products. It monetizes competition between sellers. Every seller who wants to be seen more than their competitor pays Alibaba for that privilege. And with millions of sellers, the competition never stops.

A Step-by-Step Walk Through How the Model Works

To make this concrete, here is the lifecycle of a transaction on Alibaba’s platform:

Step one: Seller lists products. A seller creates an account, sets up a storefront, and lists products. On Taobao, this is free. On Tmall, there are fees involved.

Step two: Buyer searches. A consumer searches for a product. The results they see are influenced by both relevance algorithms and paid placements. Sellers who have bid on relevant keywords appear higher.

Step three: Seller runs ads. To increase visibility, the seller activates keyword bidding and display advertising. They set a budget and pay per click or per impression.

Step four: Buyer purchases. The buyer completes a transaction via Alipay or another payment method. The funds are held in escrow until the buyer confirms receipt.

Step five: Alibaba earns. Alibaba collects revenue at multiple points: from the ad spend that drove the buyer to the listing, from the transaction commission (on Tmall), and potentially from logistics fees if Cainiao handles fulfillment.

One transaction, multiple revenue touch points.

A Real-World Seller Journey

To make this even more tangible, consider the journey of a manufacturer using Alibaba.com to reach international buyers.

A factory in Guangdong produces electronic components. They create a Gold Supplier account on Alibaba.com, paying an annual subscription fee. This gives them a verified badge and access to premium search rankings.

They list their products with detailed specifications and pricing. They activate advertising to appear at the top of search results when international buyers look for their category.

An importer in Germany finds them, initiates an inquiry, and eventually places a bulk order. The manufacturer processes the order, ships via a freight partner integrated with Cainiao, and Alibaba earns from the subscription fee, the ad spend, and potentially the logistics coordination.

The manufacturer gets international reach they could never afford to build independently. Alibaba earns from every layer of that transaction.

Competitive Advantages and Economic Moats

Alibaba’s business model is defensible for several structural reasons.

Network Effects

The more sellers on the platform, the more attractive it is for buyers. The more buyers, the more attractive for sellers. This two-sided network effect creates enormous switching costs. Replicating Alibaba’s network from scratch is practically impossible.

Seller Dependency

Sellers on Taobao and Tmall become deeply dependent on Alibaba’s advertising ecosystem. Their visibility, their revenue, and their customer relationships all flow through Alibaba’s platform. Leaving the platform means starting over. This creates strong retention.

Integrated Ecosystem

Alibaba’s platforms are deeply interconnected. A brand on Tmall might use Alibaba Cloud for their data infrastructure, Cainiao for logistics, and Alipay for payments. Each integration deepens the relationship and raises switching costs further.

Data Advantage

With billions of transactions processed, Alibaba has an unparalleled dataset on consumer behavior, purchasing patterns, and market trends. This data fuels better algorithms, better ad targeting, and better recommendations, which in turn drive more transactions and more data. It is another self-reinforcing loop.

Alibaba vs. Amazon: A Model Comparison

The Alibaba and Amazon comparison is instructive because the two companies have taken fundamentally different approaches to eCommerce.

Alibaba is platform-first. It connects buyers and sellers without owning inventory. It monetizes through advertising and fees. It scales by growing the network.

Amazon is inventory-plus-platform. Amazon buys and sells products directly (first-party), and also allows third-party sellers (marketplace). It has massive warehouse infrastructure and its own logistics network. Revenue comes from product sales, marketplace fees, and AWS.

The key difference is capital intensity. Amazon’s model requires enormous investment in warehouses, inventory, and logistics. Alibaba’s model does not. This is why Alibaba’s margins on its core commerce business can be so high relative to Amazon’s retail operations.

However, Amazon’s model gives it more control over the customer experience, which has been a competitive advantage in markets like the United States.

Alibaba vs. Key Competitors

Beyond Amazon, Alibaba faces distinct competitors in China and globally.

JD.com operates a logistics-heavy model similar to Amazon. It owns warehouses and delivery fleets, promising faster and more reliable shipping. JD competes directly with Tmall for brand partnerships and with Taobao on consumer reach.

Pinduoduo (now PDD Holdings) disrupted the Chinese eCommerce market with a social commerce model. It used group buying mechanics and deep discounts to attract price-sensitive consumers, particularly in lower-tier cities. Pinduoduo grew faster than anyone expected and forced Alibaba to respond with its own discount-focused initiatives.

Internationally, Alibaba’s AliExpress competes with platforms like Shopee, Lazada (which Alibaba owns), and increasingly Amazon in cross-border commerce.

Key Metrics to Track

For anyone analyzing Alibaba’s business, these are the metrics that matter most:

- GMV (Gross Merchandise Value): Total value of goods sold across platforms. This is the top-line indicator of platform health.

- Annual Active Consumers: The number of unique buyers transacting on Alibaba’s platforms. Growth here signals platform expansion.

- Monetization Rate: Revenue as a percentage of GMV. This shows how effectively Alibaba converts platform activity into revenue.

- Cloud Revenue Growth: Given the strategic importance of Alibaba Cloud, growth rate and margin here are closely watched.

- Seller Count and Growth: More sellers means more competition, which means more ad spend and more revenue.

Challenges and Risks

No business model is without its vulnerabilities. Alibaba faces several meaningful challenges.

Regulatory pressure. The Chinese government’s crackdown on tech platforms, which included a record antitrust fine for Alibaba in 2021, has created significant uncertainty. Regulatory risk remains elevated.

Counterfeit products. Taobao has long struggled with fake goods. This damages consumer trust and has complicated Alibaba’s relationships with international brands and regulators.

Ad cost inflation. As more sellers compete for visibility, ad costs rise. This can squeeze smaller merchants and eventually discourage participation, which would weaken the flywheel.

China market dependency. Despite global ambitions, the vast majority of Alibaba’s revenue still comes from China. Any slowdown in the Chinese economy or further regulatory action has an outsized impact.

Intensifying competition. Pinduoduo and JD.com are strong domestic competitors. Internationally, building market share is expensive and uncertain.

Future Strategy: Where Alibaba Is Headed

Alibaba’s strategic priorities point toward a few clear directions.

AI and cloud expansion. Alibaba is investing heavily in AI capabilities, both for internal use (improving ad targeting, search, and recommendations) and as cloud services sold to enterprises. This is a high-margin growth area.

Global commerce. Through AliExpress and Lazada, Alibaba is pushing into Southeast Asia, Europe, and other international markets. The ambition is to replicate the domestic flywheel globally.

Logistics dominance. Cainiao is being built into a global logistics infrastructure. If successful, this would make Alibaba’s cross-border commerce offering far more competitive with Amazon.

Data monetization. As AI capabilities improve, Alibaba’s data advantage becomes more valuable. Expect deeper personalization, better ad products, and new data-driven services for enterprise clients.

Lessons for Founders

Alibaba’s business model contains some of the most valuable lessons available for anyone building a scalable company.

Build platforms, not just products. Products have linear scale. Platforms scale exponentially because other people build value on top of them.

Monetize attention and activity, not inventory. Alibaba earns from the act of selling, not from products themselves. This keeps capital requirements low and margins high.

Create network effects from day one. Design your business so that each new user makes the platform more valuable for every other user. This is the most durable competitive advantage available.

Use advertising as a revenue engine. When you have a large, engaged audience, advertising can be extraordinarily high-margin. Alibaba built an ad business on top of a commerce platform, and that ad business became the primary revenue driver.

Expand into ecosystems, not just adjacencies. Alibaba did not just add more product categories. It added cloud, logistics, payments, and media. Each addition strengthened the core and opened new revenue streams.

Free is a strategy, not a weakness. Making Taobao listings free was a deliberate land-grab. It sacrificed short-term revenue for long-term network dominance. Sometimes the right price is zero.

Conclusion

Alibaba’s success is not an accident of geography or timing. It is the result of a deliberately designed business model that captures value at every layer of the commerce stack without ever needing to own the products being sold.

By owning the ecosystem rather than the inventory, Alibaba created a model that scales with almost no incremental cost. By monetizing seller competition rather than consumer transactions alone, it built a revenue engine that accelerates as the platform grows.

The flywheel keeps spinning. The data keeps compounding. The ecosystem keeps deepening.

That is how Alibaba makes money. And more importantly, that is why the model is so hard to replicate.

FAQs

Alibaba Group makes money mainly through advertising, commissions, cloud services, membership fees, and logistics services.

Its biggest revenue driver is advertising, where sellers pay to rank higher on platforms like Taobao.

No, Alibaba does not sell products directly.

Instead, it operates as a marketplace platform where third-party sellers list and sell products. This makes its business model asset-light, unlike Amazon, which holds inventory.

Alibaba’s main source of revenue is advertising.

Sellers on platforms like Taobao pay for visibility through keyword bidding, similar to Google Ads.

Yes, Alibaba is highly profitable.

Its ad-driven and platform-based model allows it to earn without holding inventory, resulting in high margins, especially from advertising and cloud services.

Alibaba Group → Marketplace-focused, earns from ads and fees

Amazon → Hybrid model (marketplace + own inventory)

👉 Alibaba focuses on enabling sellers, while Amazon also acts as a retailer.

Alibaba uses its logistics network called Cainiao to manage deliveries.

Instead of owning delivery systems fully, it coordinates logistics through partners, making it scalable and cost-efficient.

Alibaba’s strategy is to:

Build a platform ecosystem

Attract sellers and buyers

Monetize through ads and services

Expand into cloud and logistics

👉 It focuses on owning the ecosystem, not the inventory.

Alibaba succeeds because of:

Strong network effects

High-margin advertising model

Asset-light structure

Integrated ecosystem (commerce + cloud + logistics)

Discover more from Business Model Hub

Subscribe to get the latest posts sent to your email.