Shopee’s GMV surpassed $100 billion in 2024 with 28% growth and over 10 billion gross orders, marking its first full year of adjusted EBITDA profitability. But here’s what most people miss Shopee didn’t start profitable. It burned billions to get here.

After analyzing many of e-commerce platforms and tracking Shopee’s evolution, I’ve identified the specific mechanisms that transformed this mobile-first marketplace into Southeast Asia’s undisputed e-commerce leader with 52% market share in 2024, up from 48% in 2023.

This isn’t another surface-level “Shopee overview.” I’m breaking down the actual revenue architecture, revealing little-discussed monetization strategies, and comparing Shopee’s model against its biggest rival Lazada to show you exactly why one platform dominates while the other struggles.

The Numbers That Tell Shopee’s Real Story

Let’s start with hard data that reveals Shopee’s true scale:

2024 Financial Performance:

- Total revenue grew 37% year-over-year to $4.95 billion in Q4 2024, the fastest growth rate in nearly three years

- E-commerce segment GMV reached $23.3 billion with a year-over-year increase of 29.1%

- Marketplace take rate improved to 11.2%, up from 10.0% in Q4 2023

- E-commerce gross margins expanded by 500 basis points to 46%

Market Dominance:

- Shopee commanded $66.8 billion of Southeast Asia’s $128.4 billion e-commerce GMV in 2024

- Gross orders for 2024 totaled 10.9 billion, an increase of 33% year-over-year

- Of the $14 billion GMV added across Southeast Asia in 2024, Shopee captured $12 billion

These numbers reveal something critical: Shopee isn’t just growing it’s capturing almost all new e-commerce spending in the region while improving profitability simultaneously.

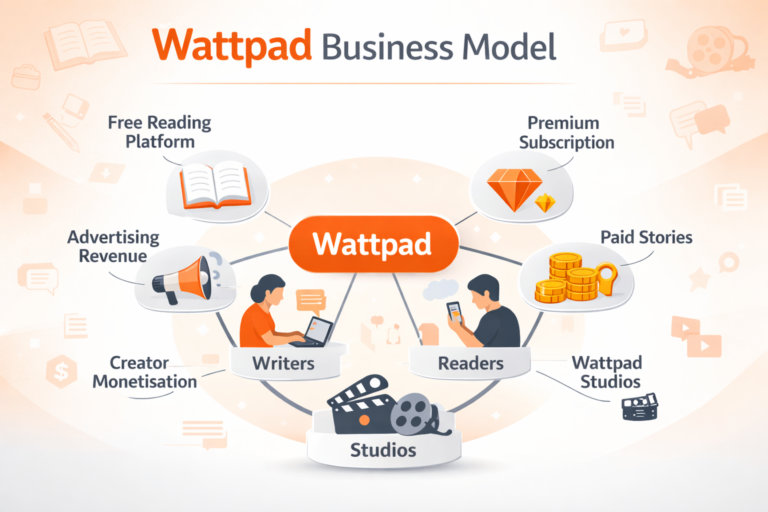

What Is Shopee? Beyond the Simple Marketplace Label

Shopee is a mobile-first e-commerce ecosystem owned by Sea Group (formerly Garena), launched in 2015 to dominate Southeast Asian and Latin American markets where traditional e-commerce giants had weak presence.

Operating in Singapore, Indonesia, Malaysia, Philippines, Thailand, Vietnam, Taiwan, and Brazil, Shopee doesn’t just connect buyers and sellers it owns the entire transaction stack:

The Complete Ecosystem Includes:

- Core marketplace platform

- Digital payment system (ShopeePay)

- Last-mile logistics network (SPX Express)

- Advertising technology platform

- Seller financing and support services

- Live streaming and social commerce features

This vertical integration is what most analyses miss. Shopee isn’t competing as just a marketplace—it’s competing as a complete commerce infrastructure.

The Shopee Business Model: Marketplace Architecture Explained

Shopee operates on a third-party marketplace model where 96% of GMV comes from third-party sellers, with only 4% from first-party sales.

How the Transaction Flow Works

Step 1: Product Listing Sellers (individual entrepreneurs, SMEs, or brands) list products on Shopee’s platform with complete control over pricing, descriptions, and inventory.

Step 2: Discovery and Purchase Buyers browse through categories, search results, or personalized recommendations powered by AI algorithms. Shopee’s interface emphasizes visual discovery and gamification.

Step 3: Escrow Payment System When buyers place orders, Shopee holds payment in escrow rather than immediately releasing funds to sellers. This critical trust mechanism addresses fraud concerns prevalent in emerging markets.

Step 4: Fulfillment Sellers ship products either through Shopee’s logistics partners or SPX Express. Shopee tracks every shipment and provides delivery guarantees.

Step 5: Payment Release After buyers confirm delivery or a predetermined period passes, Shopee releases payment to sellers minus commissions and fees.

Step 6: Post-Purchase Reviews, ratings, and potential returns are managed through Shopee’s platform, creating the feedback loop that builds seller reputation.

This escrow-based system is why Shopee succeeded where others failed in Southeast Asia—it solved the fundamental trust problem that plagued regional e-commerce.

The Seven Revenue Streams Powering Shopee’s $4.95B Business

Most people think Shopee makes money just from seller commissions. That’s only the beginning. Here’s the complete monetization architecture:

1. Marketplace Commissions: The Foundation

Shopee charges transaction-based commissions on completed sales, with rates varying by:

- Product category: Electronics might carry 2-3% commission, while fashion could be 5-8%

- Seller tier: New sellers often receive promotional zero-commission periods, while established sellers pay standard rates

- Sales volume: Higher-volume sellers may negotiate better rates

Shopee raised merchant commission fees by one-third in 2024, such as increasing the commission in Thailand from 10% to 13% in July. Critically, despite these price hikes, GMV continued growing at a mid-20% rate in the second half of 2024—clear evidence of pricing power and an economic moat.

Why This Matters: The ability to raise prices without losing sellers or buyers demonstrates Shopee has achieved true platform power—sellers can’t afford to leave because that’s where the customers are.

2. Advertising Revenue: The High-Margin Goldmine

Shopee’s advertising platform has become crucial to profitability. Ad revenue increased by 50% year-over-year, with take rates up 50 basis points.

Advertising Products Include:

Keyword Search Ads: Sellers bid on search terms to appear at the top of results when buyers search for products. This is performance-based advertising where sellers only pay when buyers click.

Discovery Ads: Promoted product placements in feeds, category pages, and homepage carousels that increase product visibility beyond organic reach.

Shop Ads: Brand-level advertising that promotes entire stores rather than individual products, helping established sellers build brand recognition.

Shopee Live Ads: Sponsored live streaming sessions where sellers demonstrate products in real-time, combining entertainment and commerce.

Why advertising is critical: Unlike commissions that scale linearly with GMV, advertising scales with seller competition. As more sellers fight for visibility, ad spending increases even if total sales remain constant. This creates margin expansion—exactly what Shopee demonstrated in 2024.

3. Transaction and Payment Processing Fees

Beyond commissions, Shopee charges service fees for:

Payment Processing: Small percentages on every transaction for handling payment logistics, fraud prevention, and fund transfers.

Currency Conversion: Fees when cross-border transactions require currency exchange.

ShopeePay Integration: While ShopeePay reduces third-party payment gateway costs, Shopee still captures value through digital wallet ecosystem lock-in.

These fees seem tiny individually (often 1-2% per transaction) but with 10.9 billion orders in 2024, they accumulate to significant revenue.

4. Logistics and Shipping Margins

This is where Shopee’s vertical integration creates hidden revenue streams.

SPX Express Advantage: By building its own logistics network, Shopee captures margins that would otherwise go to third-party couriers. Even when shipping appears “free” to buyers, sellers typically pay shipping fees embedded in Shopee’s pricing structure.

Logistics Technology: SPX Express enhancements improved service quality while reducing costs, creating both revenue opportunity and cost advantage simultaneously.

Three-Way Economics: Buyers see free or subsidized shipping (acquisition tool), sellers pay reasonable logistics fees (revenue source), and Shopee captures the margin through owned infrastructure (profit center).

5. Shopee Mall: Premium Brand Monetization

Shopee Mall is the platform’s verified brand section where official brand stores pay premium fees for:

Higher Commission Rates: Typically 2-5% above standard marketplace rates in exchange for premium positioning and trust badges.

Mandatory Advertising Spend: Many Shopee Mall merchants commit to minimum advertising budgets as part of their partnership agreements.

Service Fees: Additional fees for premium features like advanced analytics, priority customer service, and enhanced brand customization options.

Why brands pay premium: Shopee Mall provides authenticity guarantees that combat counterfeits—critical in markets where fake products are prevalent. This trust factor justifies higher fees.

6. ShopeePay and Financial Services Revenue

Shopee’s digital wallet ShopeePay generates revenue through:

Merchant Discount Rates: Businesses accepting ShopeePay payments (both on and off Shopee) pay processing fees.

Cash-Out Fees: Users transferring money from ShopeePay to bank accounts pay small fees.

Float Interest: Money sitting in ShopeePay wallets generates interest for Shopee before users spend it.

Credit Services: Through SeaMoney (Sea Group’s fintech arm), Shopee offers seller financing and buyer credit products that generate interest revenue.

Strategic Value: ShopeePay keeps users in the Sea ecosystem, increases switching costs, and provides valuable transaction data for improving recommendation algorithms.

7. Value-Added Seller Services

Shopee monetizes seller success through optional premium services:

Seller Education Programs: Paid courses and certification programs teaching sellers how to optimize listings, run campaigns, and grow their businesses.

Advanced Analytics: Premium data insights showing traffic sources, conversion optimization opportunities, and competitor benchmarking.

Enhanced Support: Priority customer service, dedicated account managers for high-volume sellers, and faster payment release cycles.

Campaign Participation: Fees for participating in major shopping festivals like 11.11 or 12.12, where sellers pay for prominent placement during high-traffic periods.

How Shopee Built Market Dominance: The Growth Strategy Nobody Talks About

Shopee’s path to 52% market share wasn’t just good product it was deliberate, aggressive strategy that prioritized growth over profits until achieving insurmountable scale.

Phase 1 (2015-2019): Burn Money to Buy Market Leadership

Shopee lost billions in its first five years by:

Subsidizing Free Shipping: Covering logistics costs that would normally be passed to buyers or sellers, removing the biggest barrier to online shopping adoption.

Heavy Discounts and Vouchers: Constant promotional campaigns that trained consumers to expect bargains, building purchase habits.

Zero Commission Periods: Letting sellers keep 100% of revenue initially to rapidly build supply-side liquidity.

Aggressive Marketing: Celebrity endorsements, TV commercials, and digital advertising that far exceeded revenue generation capacity.

Why burn money? E-commerce marketplaces have powerful network effects—the platform with more buyers attracts more sellers, which attracts more buyers. Shopee spent to reach critical mass before competitors could.

Phase 2 (2020-2022): Accelerate During Pandemic While Others Paused

COVID-19 was Shopee’s inflection point. While competitors cut spending and pulled back, Shopee accelerated investment:

Mobile-First Advantage: When lockdowns forced digital adoption, Shopee’s mobile-optimized experience captured new users competitors couldn’t reach.

Logistics Investment: Building SPX Express during the pandemic positioned Shopee to handle exploding demand while competitors struggled with third-party logistics bottlenecks.

Live Commerce Innovation: Launching live streaming shopping features earlier than rivals, tapping into entertainment-driven commerce before it became mainstream.

Phase 3 (2023-Present): Monetize Market Leadership

With market leadership secure, Shopee shifted to profitability:

Commission Increases: Raising seller fees by 30%+ because sellers can’t abandon the platform without losing access to the largest buyer base.

Advertising Growth: Pushing more sellers into paid advertising as organic reach becomes increasingly competitive.

Logistics Margins: Capturing profits from owned logistics infrastructure now that volume justifies the investment.

Reducing Subsidies: Gradually decreasing buyer discounts and free shipping programs as consumers have developed platform habits.

The result: 2024 marked the first full year of adjusted EBITDA profitability, with Asia and Brazil both now profitable.

The Complete Shopee vs Lazada Business Model Comparison

Understanding why Shopee dominates while Lazada struggles requires comparing their strategic approaches side-by-side.

Market Position and Scale

Shopee:

- 52% market share in Southeast Asia in 2024, reaching $66.8 billion GMV

- Gross margin improved to 45%, with e-commerce margins at 46%

- First full year of profitability achieved in 2024

Lazada:

- Market share declining under pressure from Shopee and TikTok Shop

- Achieved positive EBITDA for the first time in July 2024, twelve years after founding

- Aims to achieve annual GMV of $100 billion by 2030 (target Shopee already hit in 2024)

Key Difference: Shopee achieved in 9 years what Lazada is projecting for 15 years. This isn’t just about execution—it reflects fundamentally different strategic priorities.

Monetization Strategy

Shopee:

- Take rate of 11.2%, up from 10.0% in Q4 2023

- Ad revenue increased 50% year-over-year

- Aggressive pricing power through commission increases that stick

Lazada:

- Takes sales fees of 1 to 4% on marketplace transactions

- Lower monetization reflecting weaker market position

- Cannot raise prices without risking seller exodus to Shopee

Key Difference: Shopee can charge 11%+ because sellers need access to its massive buyer base. Lazada’s 1-4% rates reflect weaker bargaining position—sellers have alternatives.

Technology and Infrastructure

Shopee:

- Mobile-first platform built for Southeast Asian smartphone users

- Owned logistics network (SPX Express) providing both cost advantage and control

- Integrated payment system (ShopeePay) capturing financial services revenue

- Advanced AI-powered recommendation and advertising systems

Lazada:

- Desktop origins requiring retrofitting for mobile

- Multiple legacy complexities dating from Rocket Internet days (2012-2016), where different cultures and expectations were layered on top of each other

- Efficiency improvements through AI-enabled operations, online marketing, user incentives and optimized logistics services

- Fighting to modernize inherited infrastructure

Key Difference: Shopee designed mobile-first; Lazada adapted from desktop. This architectural difference affects every aspect of user experience, conversion rates, and operational efficiency.

Parent Company Strategy

Shopee (Sea Group):

- Part of integrated gaming (Garena) + e-commerce (Shopee) + fintech (SeaMoney) ecosystem

- Single regional focus with consistent execution

- Patient capital allowing multi-year investment in market leadership

Lazada (Alibaba):

- Alibaba made at least ten investments totaling nearly $8 billion since 2016

- Operates local marketplaces in six distinctive markets where supplies must be organized locally in each market

- Resource allocation challenges competing with Alibaba’s other international priorities

Key Difference: Shopee is Sea’s crown jewel receiving full support. Lazada competes for attention within Alibaba’s global portfolio, leading to less consistent investment and strategic direction.

Go-To-Market Philosophy

Shopee:

- Mass market approach targeting all consumer segments

- Emphasis on C2C (consumer-to-consumer) and SME sellers

- Gamification, entertainment, and social features driving engagement

- Aggressive user acquisition regardless of short-term losses

Lazada:

- Repositioned to focus on high-quality assortments, AI-driven logistics, and premium sellers, moving away from direct competition with Shopee in the value segment

- Carving a niche in higher-end goods rather than competing head-to-head

- More conservative spending after years of losses

Key Difference: Shopee bet everything on winning mass market. Lazada is retreating to premium positioning—a strategy that might enable profitability but concedes market leadership.

Profitability Timeline

Shopee:

- 2015: Launch

- 2015-2023: Heavy losses while building market position

- 2024: First full year of profitability while maintaining growth

Lazada:

- 2012: Launch (3 years earlier than Shopee)

- 2012-2024: Losses for twelve consecutive years

- July 2024: First monthly profit

- Still seeking sustained profitability

Key Difference: Shopee spent aggressively but transitioned to profitability from strength. Lazada’s profitability comes from cutting costs and retreating from competition, not from dominant market position.

Why Shopee’s Business Model Works (And Lazada’s Struggles)

The fundamental difference isn’t features or technology it’s strategic coherence.

Shopee’s Winning Formula:

- Scale-First Economics: Spent massively to achieve overwhelming market share, then monetized from position of strength

- Mobile-Native Design: Built specifically for emerging market mobile users, not retrofitted from desktop

- Vertical Integration: Owned logistics and payments creating cost advantages and revenue streams competitors can’t match

- Consistent Strategy: Never wavered from mass market dominance goal despite years of losses

- Network Effects: Reached the tipping point where buyers and sellers can’t leave without losing value

Lazada’s Strategic Handicaps:

- Early Mover Disadvantage: Being first meant building on assumptions (desktop focus, inventory model) that later proved wrong

- Inconsistent Ownership: Multiple organizational changes under Alibaba created strategic whiplash

- Resource Constraints: Despite $8 billion investment, never had the sustained, focused support Shopee received

- Structural Complexity: Operating six separate country marketplaces increased costs and reduced efficiency

- Competitive Response Too Slow: By the time Lazada mobilized serious competition, Shopee had unassailable lead

Shopee’s Cost Structure: Where the Money Goes

Understanding costs reveals why profitability took so long and why it’s now sustainable:

Major Operating Expenses:

Technology Infrastructure: Platform development, server costs, AI/ML algorithm improvements, mobile app maintenance, and cybersecurity significant ongoing investment to handle billions of transactions.

Marketing and User Acquisition: TV commercials, digital advertising, influencer partnerships, and promotional campaigns. Sales and marketing spending generated higher returns due to ad tech improvements and SPX Express enhancements.

Logistics Subsidies: Even with owned logistics, Shopee still subsidizes shipping costs to maintain competitive advantage, though less than in growth phase.

Payment Processing: Infrastructure for handling ShopeePay transactions, fraud prevention systems, and payment gateway fees for non-ShopeePay transactions.

Customer Service: Multi-language support teams across all markets handling buyer inquiries, seller support, and dispute resolution.

Seller Incentives: Promotional programs, voucher systems, and commission discounts for strategic sellers or product categories.

The shift to profitability came from:

- Marketing spending becoming more efficient as brand recognition reduced customer acquisition costs

- Owned logistics reaching scale where cost per delivery dropped below third-party alternatives

- Reduced need for heavy discounts as habit formation took hold

- Advertising revenue growing faster than platform costs

Category Performance: Where Shopee Makes Most Money

Fashion contributes the most (32%) to Shopee GMV, with electronics as the second biggest category at 27%.

Understanding category economics reveals monetization nuances:

High-Volume, Lower-Margin Categories:

- Fashion and accessories: Highest GMV but lower commission rates (5-8%) due to intense competition

- Electronics: High ticket prices generating significant GMV despite lower margins

High-Margin, Strategic Categories:

- Beauty and personal care: Higher commission rates (10-15%) and strong advertising spend from brands

- Home and living: Solid margins with less price sensitivity than electronics

Growth Categories:

- Groceries and fresh food: Currently subsidized for growth, future revenue opportunity

- Digital products: Software, subscriptions, and gift cards with minimal logistics costs

This category mix is why Shopee can maintain 11%+ take rates—the blend of high-volume and high-margin products averages out to strong overall monetization.

The Future of Shopee’s Business Model: What’s Next?

Based on current trajectory and market dynamics, here’s where Shopee is heading:

1. Continued Margin Expansion

With market leadership secure, expect further monetization increases:

- Additional commission rate hikes, especially in categories where Shopee has pricing power

- Heavier push into advertising as sellers compete for visibility

- Value-added services becoming meaningful revenue contributors

- Logistics margins improving as SPX Express reaches optimal scale

2. Fintech Integration Deepening

ShopeePay and SeaMoney will become larger revenue drivers:

- Seller financing and working capital loans

- Consumer credit products (buy now, pay later)

- Cross-border payment solutions

- Insurance and investment products

3. Live Commerce and Social Features

The line between entertainment and commerce will blur:

- More sophisticated live streaming tools with better monetization

- Social features creating viral product discovery

- Creator partnerships where influencers get shops and revenue shares

- Gamification driving habitual app opening beyond purchase intent

4. Automation and AI

Technology will reduce costs while personalizing experience:

- AI-powered customer service reducing support costs

- Automated inventory management for sellers

- Hyper-personalized recommendations increasing conversion

- Predictive logistics reducing delivery times and costs

5. Geographic Expansion vs. Consolidation

Strategic choice ahead:

- Expansion option: Enter new markets (India, Middle East) replicating Southeast Asian success

- Consolidation option: Deepen penetration in existing markets, increase frequency and basket size

Given profitability focus, consolidation seems more likely—better to dominate eight markets completely than spread resources thinly.

Key Lessons from Shopee’s Business Model

For entrepreneurs, investors, and strategists, Shopee’s story offers critical insights:

1. Timing Matters as Much as Product

Shopee launched at the perfect moment when:

- Mobile internet penetration reached critical mass in Southeast Asia

- Consumers gained confidence in online shopping

- Payment infrastructure existed but wasn’t locked to competitors

- Logistics networks were developing but not yet monopolized

2. Growth Doesn’t Equal Profitability (Initially)

Shopee burned billions establishing market leadership before optimizing monetization. The sequence matters—dominant position first, then profit extraction.

3. Marketplace Power Is Binary

Being #1 isn’t slightly better than #2—it’s exponentially better. Network effects mean the leader captures disproportionate value. This justified Shopee’s aggressive spending.

4. Own Your Critical Infrastructure

Shopee’s investments in SPX Express and ShopeePay created defensible advantages competitors can’t easily replicate. Vertical integration adds complexity but pays off at scale.

5. Mobile-First Isn’t Mobile-Also

Building natively for mobile rather than adapting desktop experiences created fundamental advantages in user experience, loading speed, and conversion that Lazada couldn’t overcome.

6. Pricing Power Comes From Necessity, Not Features

Shopee can raise commissions 30%+ because sellers need access to its buyers. Lazada can’t raise prices because sellers have alternatives. Market position determines pricing power.

7. Local Execution Beats Global Templates

Despite regional platform, Shopee customizes for each market’s unique preferences, payment methods, and logistics realities. Cookie-cutter approaches fail in diverse regions.

The Bottom Line: Why Shopee’s Model Works

Shopee’s business model succeeds because it solved the fundamental challenges of emerging market e-commerce:

Trust Problem: Escrow payments and buyer protection policies addressed fraud concerns that prevented online shopping adoption.

Logistics Problem: Invested in owned delivery infrastructure when third-party logistics couldn’t handle e-commerce volume or reliability requirements.

Discovery Problem: Mobile-first design with visual discovery, live streaming, and social features matches how Southeast Asian consumers naturally shop.

Access Problem: Enabled millions of small sellers to reach national audiences without needing inventory, storefronts, or sophisticated operations.

Payment Problem: ShopeePay and COD options served markets where credit card penetration is low and trust in online payments was building.

The result is a platform that captured 52% of Southeast Asia’s e-commerce market while achieving profitability and maintaining 28% growth proof that the business model doesn’t just work theoretically, but creates sustainable competitive advantage in practice.

For anyone studying platform business models, marketplace economics, or emerging market strategy, Shopee is a masterclass in building winner-take-most network effects through patient capital, aggressive expansion, and eventual disciplined monetization from an unassailable position.

Discover more from Business Model Hub

Subscribe to get the latest posts sent to your email.

[…] vs Shopee (Quick […]